In House Bank Summary

To optimize liquidity and reduce expenses associated with cash management and financing within a group one solution is to deploy an In House Bank. The benefits of an In House Bank are shown in the graph.

This article describes what an In House Bank looks like by providing a practical example of how it can be deployed in an organization.

In the example provided the In House Bank caters for the payments to our vendors and for registration of bank statements. Next to this, intercompany payments are being facilitated in the In House Bank. We see how the benefits are being realized for the organization deploying an In House Bank.

The setup of an In House Bank is typically not something that is done overnight. The good news is that it can be rolled out in phases for those organizations that find this is the better implementation path for them. With a rollout implementation the organization is able to learn while implementing and rolling out the system without adding too much stress on existing resources. Other organizations prefer the big bang implementation which for them has the advantage to be able to reap the benefits in a sooner stage. The most optimal implementation is always determined by the organization.

Treasury Improvement can help in deploying an In House Bank in your organization. Contact us to discover the possibilities in your organization.

In House Bank benefits

What is In House Bank?

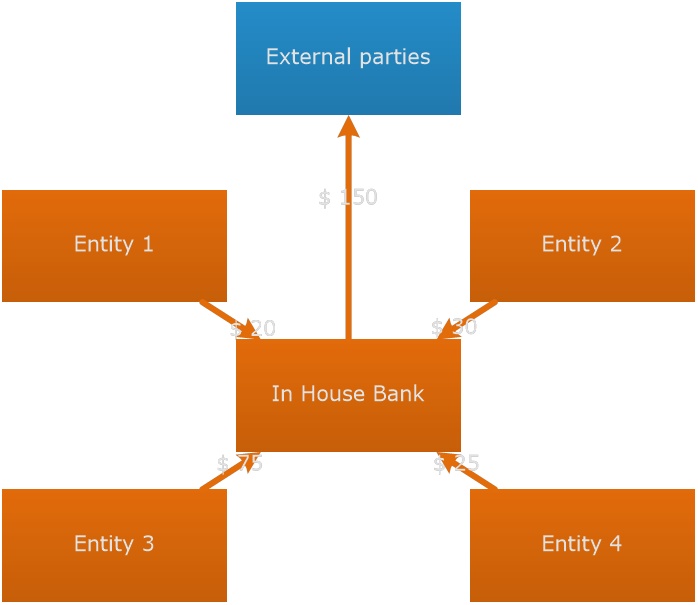

The In House Bank (further “IHB”) is an internal bank that sits between the entities of the group and the external bank. In this example all entities are dealing with the IHB. The IHB deals with the external bank. So, instead of each entity doing business with the external bank, everything now goes through the IHB. The IHB collects all payment requests from the entities, groups them and then sends them to the external bank. The statements are received from the external bank and handled by the IHB for all entities.

Intercompany payments and receipts

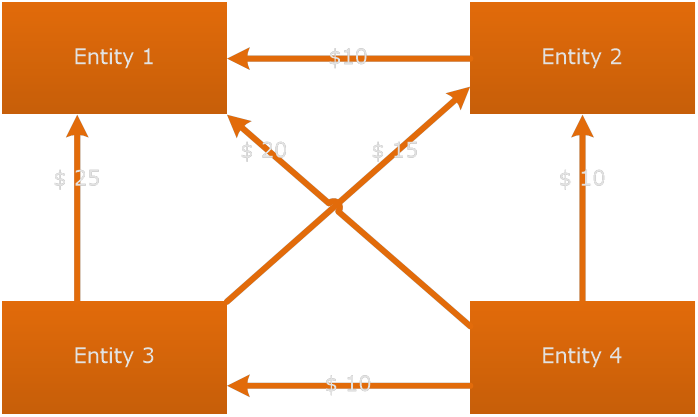

Intercompany transactions can go through the IHB. Within a IHB setup, cost savings are realized by eliminating physical cash flows. Consider the first situation, in which Entity 1 has to pay $10 to Entity 3 and at the same time Entity 3 has an obligation to pay Entity 1 $35. Also other receivables/payables relations may exist as shown in the first picture.

Without IHB all these payments will be made separately from each other, incurring lots of transaction costs. By netting the cash flow streams between the entities in the IHB cost savings are realized on the transaction costs. This is visualized in the second picture.

Off course this is a first step to saving quite some money annualy. But it can be optimized even further, by establishing the cash pool concept.

The IHB ‘collects’ all the money and determines the net position that each entity has to receive in the cash pool. In this example Entity 3 had to pay $25 to Entity 1 and $15 to Entity 2 and receive $10 from Entity 4.

The IHB functions as an intermediary in the organization to eliminate physical cash flows. In the IHB there will not be any physical cash flows between entities. Instead, accounting entries will be made to reflect the balances between the entities. These accounting entries are performed in the administrations of all entities.

In the example this comes down to Entity 1 having a $25 receivable from Entity 3, a $10 receivable to Entity 2 and a $20 receivable from Entity 4. Also the other entities will have balances with each other reflected in their books. In total Entity 1 has IHB receivables of $55.

A total of 12 bank transfers has been reduced to 0. Even more so, no money is being trapped anymore in the organization. Remember that in the beginning situation Entity 1 actually had to pay $70 to the other intercompany parties. This $70 would have been needed to be drawn from the bank and possibly even had to be borrowed to make the payments in the first place. The liquidity drain in intercompany transactions is often underestimated for.

External payments and receipts

External payments to vendors are made out of the central payment account of the IHB.

The payments that are made to external vendors all go through the IHB. The IHB first collects all payment requests from the entities. The second step is to perform a central payment run after the IHB has collected all the data from the entities. In this step the payments will be grouped as much as possible. With the central payment run a file is created which is sent to the external bank for processing and the vendors are paid.

Especially the possibility to group payments will reduce the volume of payment transactions executed by the external bank. This leads to direct cost reductions for payments made.

Another benefit is that the central payment run can be controlled much better leading to a significant improvement in the cash forecasting process on the outflow side.

Setup of In House Bank

As stated, there is no money flowing in the intercompany settlement in the IHB. The real money is at the owner of the IHB. This means that the IHB entity has external bank accounts in which the money is available, which is called the Master account. The other entities may also have external bank accounts, but these are typically only used for collecting money from their local customers or for specific local reasons. These bank accounts are called local collection accounts. The money they collect will be transferred automatically to the bank accounts of the IHB. This is called the zero balancing concept. This happens automatically every day in the day-end process. This makes sure that all the collection accounts in the local entities have a balance of 0,00 at the end of the day. The money is then transferred to the account of the IBH. At the moment the money is transferred there is an intercompany payable by the IHB to the other entities.

As explained, outgoing payments are executed from one central bank account, owned by the IHB owner. This is called the disbursement account. When a vendor of an entity is paid from the disbursement account, then this transaction results in a receivable from this entity in the books of the IHB. If the IHB owner pays a vendor of a local entity then the IHB has a receivable towards the local entity. At the same time the local entity has a payable towards the IHB.

An example of a bank account structure is as shown in the graph. Depending on the needs, wants, local limitations the structure can look differently. This will be tailored to the circumstances in the In House Bank project by Treasury Improvement.

Foreign exchange rate in the In House Bank

When entries in the IHB are made which are in a currency other than the default currency, then rate of exchanges are used. This is to translate the foreign currency amounts to company code currency amounts. In the IHB the rate of exchange is used based on the posting date of the entry. The rate of exchange is typically advised by the central Treasury department in an internal foreign exchange deal.

This use of foreign exchange rates in the IHB eliminates the need to trade foreign exchange for intercompany transfers within the organization.

Tax and Legal implications

Setting up an IHB in an international organization brings with it certain tax and legal implications based on amongst others the jurisdictions in which the various entities are located. Some of the items that need to be clarified are for example thin capitalization rules which may have an impact, currency controls in certain jurisdictions or limitations in intercompany setups between blacklisted countries.

In any case proper intercompany documentation must be setup to document the relationship and the nature of the IHB which includes at arms lengths pricing.

The IHB is first and foremost a solution to reduce total cost of (international) cash management but may be utilized in an organization's tax planning as well.

From a legal, regulatory and control perspective the IHB helps organizations to get control over payment flows and bank accounts within the group. This has a mitigating effect on the risk of fraud.

Conclusion

An IHB is capable of significantly reducing cost of international cash management in organizations. On top it frees trapped intercompany cash usage and has the potential to reduce total gross borrowing due to elimination of borrowing for intercompany payments.

In organizations with multiple subsidiaries the setup of an IHB makes much sense:

- Reduction of cost

- Increase of control

- Risk mitigation

For those organizations already having an In House Bank active there are add-ons possible to further streamline the cash flow and optimize operations.

Imagine the In House Bank buying the accounts receivables and collecting directly from the clients in an internal factoring programme. Read more on the possibilities in the case study on Factoring. For further information on arms length pricing read the article on Intercompany Credit Ratings Modelling.